Guide to Wildfire Risk

Everything you need to know about managing wildfire risk

As wildfires become more and more common, managing your risk is extremely important.

How do wildfires happen?

Not all fires are the same. Some are big, some are small. Some burn for days or weeks while others are extinguished in a matter of hours. One thing remains the same: they have the horrifying ability to ruin lives, flatten property and leave a trail of destruction in their wake.

But just where do wildfires come from? How do they happen in the first place?

According to a 2017 study that analyzed roughly 1.6 million wildfires that occurred between the years 1992 and 2012 in the United States, 84% of wildfires were caused by people. However, the same study concluded that human-caused fires only accounted for 44% of the total acres burned. In other words, naturally ignited wildfires accounted for only 16% of the total fires but for more than half the acres burned by those fires.

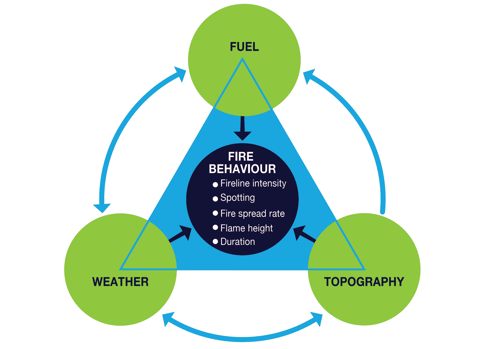

Regardless of the source of ignition, be it an improperly maintained campfire or a bolt of lightning striking a dry hillside, wildfires require adequate environmental factors to successfully burn, including available fuel, dry conditions, wind, and warm temperatures. Fire scientists have a simple model to understand what fires need to ignite: a fire triangle.

A fire triangle represents three major factors that affect wildfire behavior:

(1) Weather: relative humidity, wind precipitation, and atmospheric stability.

(2) Fuel: how much fuel there is and how dry it is.

(3) Topography: elevation, slope and aspect (the direction a given piece of land is facing).

In conjunction with optimal environmental conditions, wildfires grow thanks in part to embers – burning pieces of airborne wood or vegetation that float through the air and allow the fire to grow larger and larger. Embers can cause wildfires to spread not only quickly but also unpredictably, causing logistical problems for firefighters and resulting in larger conflagrations and more potential destruction.

Wildfires are not fun. Unfortunately, they are becoming increasingly common.

The Western U.S. has seen numerous extreme wildfires in recent years.

Increasing risk

Since 1950, 11% of the total land in the Western U.S. (defined as Washington, Oregon, Idaho, Montana, Wyoming, California, Nevada, Utah, Colorado, Arizona and New Mexico) has burned – that is over 100 million acres, or an area roughly the size of California. Though 11% of the total land burned over the course of over 70 years does not sound that bad, the frequency and annual amount of land burned is increasing.

Recent years have seen tens of thousands of fires per year burn millions of acres of land in the West. In 2020 alone, over 10 million acres burned (roughly 1% of the total land in the Western U.S.) to the tune of just under $20 billion in damages: 37 people lost their lives and more than ten thousand buildings were razed to the ground.

But why are wildfires becoming more frequent and why are more and more people being affected? There are two reasons: a warming climate and a shifting population.

Climate change has created favorable fire conditions, allowing forest fires to happen more frequently and burn more intensely. NASA analyzed satellite data collected over two decades combined with forestry data to identify several key ways climate change is increasing the likelihood of wildfires:

- Drier weather allows accumulated fuels to become more prone to burn, giving wildfires the ability to spread rapidly.

- Higher temperatures at night do not slow wildfire spread as well as cooler nighttime temperatures.

- Warm weather makes lightning storms more likely.

- Longer warm seasons lengthen the window of time fire can occur.

Not only are environmental factors increasing the frequency and intensity of wildfires, but patterns of migration have put more people in harm's way. As a growing number of people are moving to the wildland-urban interface (WUI), a zone of transition between unoccupied wilderness and land developed by human activity, more and more people are feeling the effects of wildfire.

Warmer weather, more fires

Fueled by the evolving nature of a changing climate, drought is ravaging the western half of the United States as water supplies dwindle in an area stretching from the Pacific Ocean to the Missouri River.

Scientists have been closely monitoring the developing situation since 2000. The current mega-drought, exacerbated by recent heatwaves, has been classified as the worst regional drought in 1,200 years. Many scientists are predicting the drought will continue to worsen, meaning the potential for serious wildfire-related losses will likely grow.

Drought creates ideal conditions for wildfires to ignite and spread, putting life and property at increased risk. The threat of wildfire grows as drought conditions worsen and more moisture is pulled out of vegetation and forests. Wildfire fuels like grass, underbrush, shrubs and trees dry out and become more flammable, increasing the possibility of ignition.

18 regions in the Western U.S. are experiencing an increasing threat from wildfires due to the convergence of vulnerable vegetation zones and intense drought conditions. These areas, known as double-hazard zones, cover extensive portions of the country, heightening the risk of wildfires. Growing populations in these double-hazard zones, in tandem with increasing wildfire activity, puts life and property at risk.

Living on the edge

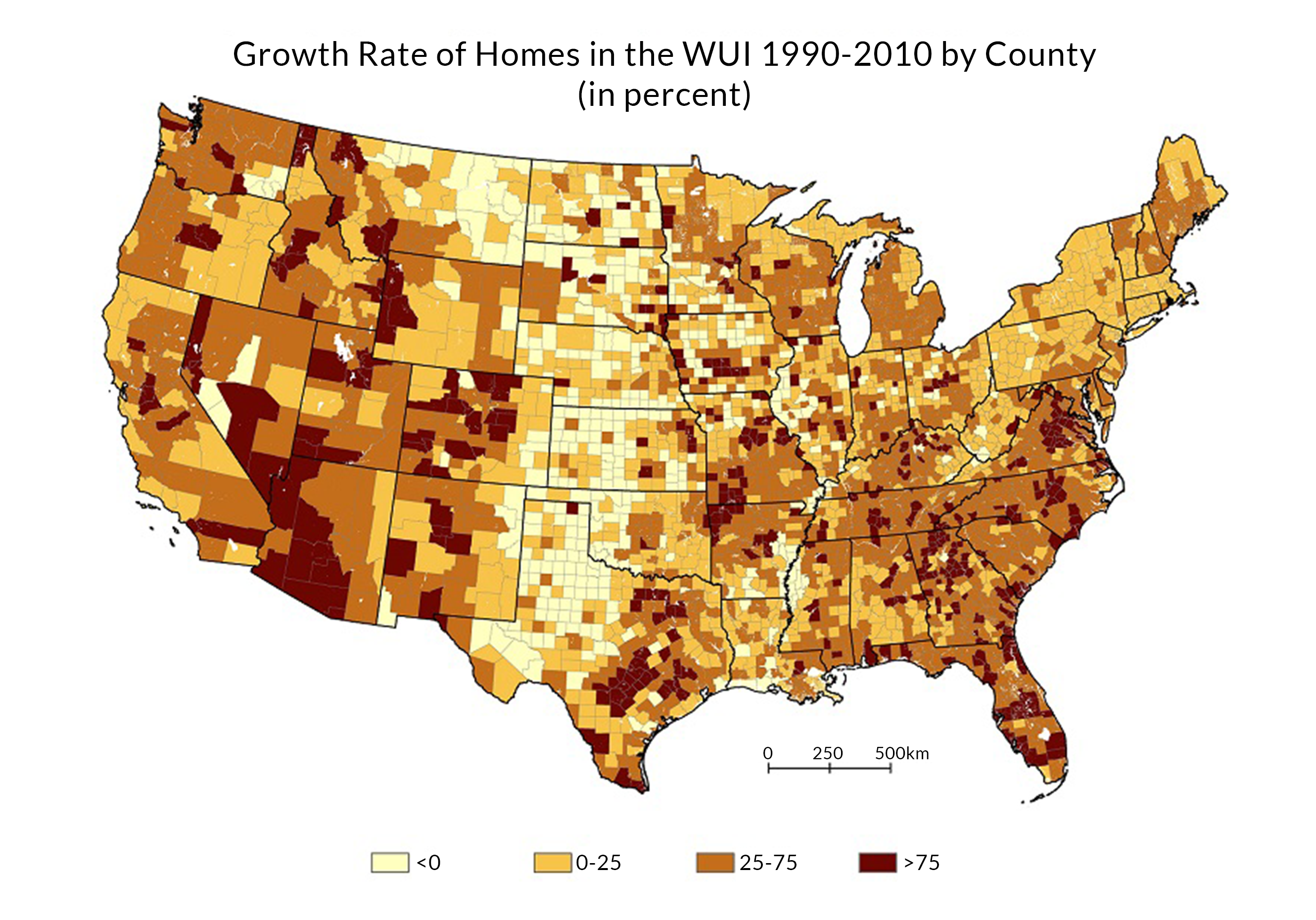

The WUI is growing faster than ever before. Between 1990 and 2010, the contiguous U.S. saw the WUI grow by roughly 73,000 square miles (an area larger than the entire state of Washington) with 12.7 million homes and 25 million added.

In conjunction with the increased frequency of wildfires, the growing development of the WUI has begun to escalate the rate of wildfire-related property damage. When more homes are built in the WUI and more people are living near areas prone to wildfire, more structures are at risk of damage if a wildfire starts.

Here is an example of WUI development in North Bend, WA.

Furthermore, the large numbers of people moving into double-hazard zones, WUI areas that suffer from heightened levels of dryness, only add to the total amount of wildfire-exposed property. Nearly 1.5 million people packed up and settled in regions known as double-hazard wildfire zones between 1990 and 2010.

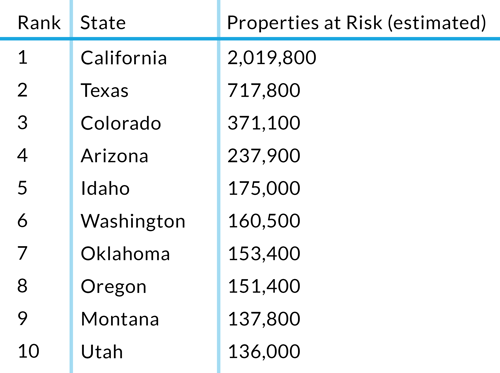

Here is a list of the top 10 states for wildfire risk and the number of exposed properties in the WUI as of 2019:

WUI development also contributes to the skyrocketing regularity of wildfires themselves. Human activity causes most wildfires and more development near wildlands means more potential for wildfire-igniting behavior. The DNR estimates 70% of wildland fires started in Washington state between 1992 and 2015 were caused by humans. Unattended campfires, improperly disposed of cigarettes, debris burns and arson are the most common reasons wildfires start.

Check out our very own Cristina Pellett's account of escaping a wildfire in 2018 to see how harrowing living in the WUI can be.

As the WUI grows — and wildfire risk grows along with it — insurance professionals are likely to need more and better information about it. It’s time to talk about what you can do to effectively manage wildfire risk.

Managing risk

The American west will continue to see wildfires for the foreseeable future. Though there are things that can be done to reduce the chances of wildfires altogether, including controlled burns, it is imperative that insurance companies take steps to effectively manage wildfire risk as fires become more volatile and unpredictable.

Risk saturation can arise for a few reasons:

- Underwriters, who operate relatively independently, can lack clear visibility into the properties their colleagues are writing. Each underwriter might only take on a small amount of risk in any given wildfire-prone region. However, the total amount taken on by the company can be difficult to gauge.

- Traditional tools, like spreadsheets, don’t clearly indicate levels of risk saturation. When an underwriter is considering a new policy, it’s time-consuming to use a spreadsheet to analyze the property’s location relative to the location of existing policies.

- Historically, insurers have relied on their reinsurers to help them measure and manage their concentration of risk, also referred to as risk saturation. But this approach, which involves infrequent (annual or semi-annual) checks of a book of business, leaves large amounts of time for risk to accumulate.

Maps help insurers overcome all these challenges and quickly see, assess and act on risk saturation.

As the saying goes, a picture is worth a thousand words - for an insurer, the right map is worth a thousand data points. Let’s explore a couple of maps together to gain a basic understanding of why they can be the difference between successfully managing risk saturation and not.

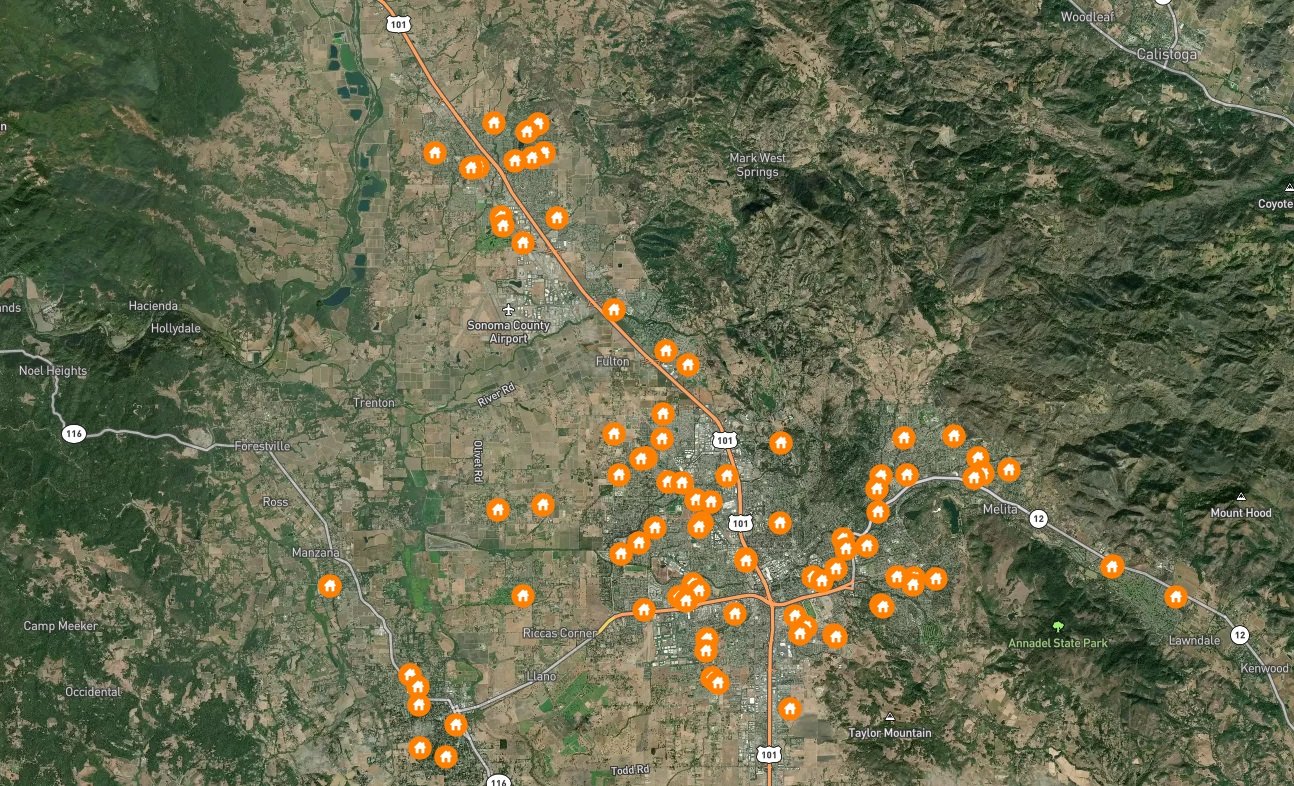

Welcome to Santa Rosa, California.

Each orange house icon below represents a single property in a simulated insurer’s book of business. Right away, you can see where you have primarily written policies - near the center of town, where the highways meet and where wildfire risk is likely lower, or on the outskirts, where wildfire risk is likely higher.

We can pair this data with another geospatial layer and make the map even more useful.

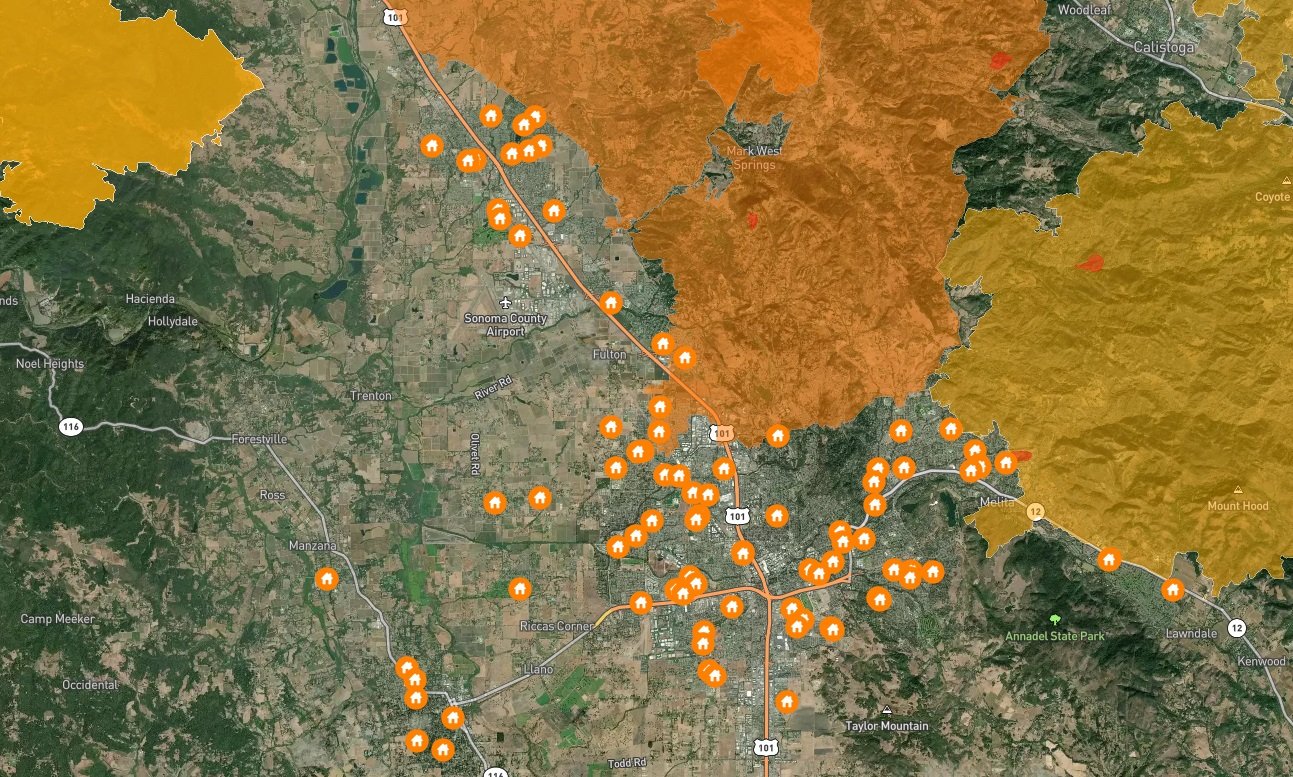

Here is the same location and the same set of insured properties now paired with the perimeters of recent wildfires. Between 2010 and 2019, two fires burned north of Santa Rosa: the Kincade fire in 2019 and the Tubbs fire in 2017.

This visualization shows you where you’ve written policies compared to where wildfires have burned in the past, indicating which properties are at the greatest risk and, more generally, how fire-prone the region as a whole is.

With maps, it requires just a few moments to take in and analyze this data versus trying to review multiple spreadsheets - they give you the ability to assess your wildfire risk concentration and determine the next best step for your business rapidly and accurately.

Ultimately, many insurers are not as proactive as they could be. Because natural disasters don’t play by the rules, managing risk saturations requires an up-to-date picture of emerging risk as it’s happening. That’s where we step in.

Pinpoint wildfire danger and effectively manage risk using

Pinpoint wildfire danger and effectively manage risk using

the BuildingMetrix Wildfire Risk Tool.

Wildfire Risk Tool

Given the right tools, property insurers can efficiently and accurately understand their concentration of risk, giving them the ability to take action to address it before it becomes a problem. To assess true loss potential, insurers need a clearer picture of risk aggregation to prevent over-saturation.

Geospatial mapping technology helps insurers visualize the location of risks and their proximity to each other, offering a more complete look at exposure and creating opportunities to improve risk management. Ultimately, location-based data improves property insurance underwriting, saving underwriters valuable time and improving their overall accuracy.

The BuildingMetrix Wildfire Risk Tool shows you two key pieces of geospatial data for every property, displayed visually on a map. The first piece of data is whether the property is in the WUI and the second is whether past wildfires have occurred nearby. These two essential elements are what give insurers a precise idea of their concentration of wildfire risk.

But how can we be sure that historical wildfire data can accurately reveal potential risk?

Certain parts of the Western U.S. are not just prone to wildfire; they experience it frequently. Research shows that some areas burn, on average, every seven years, and other research indicates the buildup of vegetation drives these repeat wildfires. By taking this historical wildfire data and matching it with properties that exist within your book of business, you can quickly see your concentration of risk in wildfire-prone areas.

To learn more about how historical wildfire perimeters can indicate future risk, check out our article on the subject.

How does the Wildfire Risk Tool work?

The “mapplication” works like popular mapping apps, allowing you to visualize all the data from your book of business in real-time. No extensive training is needed, giving you the opportunity to rapidly realize value and manage risk with ease and accuracy.

In addition to manually inputting your book data, we offer a book review - you’ll receive data on all the addresses you insure in the continental U.S. so you can quickly assess where you’ve taken on significant amounts of wildfire-related risk.

A book review can also enhance your reinsurance reviews - when you identify potential concentration of risk issues and proactively mitigate them before you meet with your reinsurer, you'll be thoroughly prepared for the review.

Learn more about how our tool works here.

Help your customers protect their homes by educating them on their wildfire risk.

Help your customers protect their homes by educating them on their wildfire risk.

Wildfire safety for customers

Insurers play such an important role in helping educate their customers. When insurance professionals know more about the science behind wildfires, they can better understand the risk to specific properties and further help their customers in meaningful ways.

Determine your at-risk customers

Wildfire Risk Tool

Using our Wildfire Risk Tool, insurance agents can identify at-risk customers. Just enter an address or latitude-longitude for any location and you will be clearly shown whether or not a given address is at heightened risk of wildfire. From there, you can begin to educate your customers, helping them mitigate the risks posed by wildfire.

Wildfire Hazard Potential

Wildfire Hazard Potential (WHP) helps identify areas of heightened risk, giving you the ability to pinpoint customers in your book of business who live in hazardous areas.

WHP is a publicly available data source originally designed for forest managers and policy makers to help them make decisions about where to deploy resources. Now, there is a community version of it you can share with your customers to help them understand their wildfire risk.

Fire scientists developed the WHP in response to the growing need for information about wildfire risk. On their website, they offer an interactive map where you can search for a community and explore information about relative wildfire risk in addition to educational resources to help homeowners understand wildfire risk and reduce their exposure.

Tips for at-risk customers

This section provides you with helpful information on how to educate your at-risk customers.

Myths

To start, it is important to address three myths about wildfires.

Myth #1: My home will only catch on fire from flames burning right up to the structure.

Research shows that embers are a primary cause of homes catching on fire. When they land on combustible material near your home, they can spread a fire onto your property and put your home at risk of burning down.

Myth #2: The fire department will be able to protect my home, even during a large wildfire.

Some wildfires grow so large with such intensity that the fire department may not have enough resources to protect every home. Preparing your home beforehand can mean the difference between your home being saved or not.

Myth #3: I only need to take steps to protect my home from wildfires once a year.

Wildfire preparedness is not a once-and-done project; it is an ongoing process. Maintaining your home and the space around it is just one part of that process.

Preparing your home

Homes at the greatest risk are those in the WUI, the transitional space between wildland and human development. Here are some important tips for preparing your home for a wildfire event.

Tip #1: Build defensible space around your home

Clear away brush and debris around your home, keep plants watered and use fire-resistant plants around your property. Learn more by watching this short video and referencing the NFPAs guide to preparing your home for wildfire.

Tip #2: Protect your roof

Build or re-roof your house with fire-resistant material, clear away pine needles/leaves and install screens on chimney openings to discourage flying embers.

Tip #3: Harden your home

Homes can be made with a variety of materials, all of which fall into one of three categories: combustible, ignition-resistant and noncombustible. A home hardened against wildfires is built with ignition-resistant (like treated lumber) and noncombustible materials (like metal and stucco) that are less likely to ignite and burn. Here is a helpful guide to retrofitting your home with fire-resistant materials.

Tip #4: Keep the inside of your home safe

Install smoke detectors, have fire extinguishers on hand and use flame-retardant fabric for drapes. Check out our guide to general fire safety for more information.

Protecting your community

Everyone who lives in a wildfire-prone area has a role to play in reducing risk – it is a community effort. After all, when wildfires occur what happens on one property can quickly affect others nearby.

The NFPAs Wildfire Community Preparedness Day, which happens each year towards the beginning of May, aims to encourage people living in wildfire-prone areas to take some of the many proactive, science-based steps that help reduce wildfire risk. In some places, a group of neighbors get together and lead the day; in others, a city council, homeowners association or other local organization takes on the leadership role.

Interested in learning more?

We’re here to help you understand and mitigate your wildfire risk - talk to one of our amazing risk data experts.